Legal Disclaimer:This post is not financial advice. It is intended for educational purposes only. Consult with your financial advisor or a certified financial professional for guidance on investment choices.

At the end of 2021, an editor acquaintance of mine reached out to me about a new opportunity regarding personal finance and entrepreneurship journalism.

“We’re seeing a lot of energy in this space,” he said. “You seem to be plugged into this world. And I’ve seen your bylines over the years. Would you like to have a conversation?”

Three months and seven interviews later, I was the newest senior editor at NextAdvisor, in partnership with TIME, overseeing the launch and direction of a new vertical all about the financial independence movement. Overall, we shepherded over 125 articles about FIRE onto TIME.com before the partnership ended in early 2023.

Byline from NextAdvisor's TIME.com partnership from 2022.

From wild side hustles to frugality enthusiasts, the people I met and interviewed helped me realize that the financial independence movement isn’t all get-rich-quick maniacs. It’s actually a movement that many of us are already participating in, whether we realize it or not.

If you’re setting income goals, taking on an online business or freelance work, and/or saving money for a future career shift, surprise: You’re a part of the FIRE movement.

The FIRE Movement: Controversial, Inspiring and Sometimes Bizarre

In this time, I learned a lot about the FIRE movement. Some components, such as making more money via the internet, were in my wheelhouse from years of being a self-employed consultant. Other components, such as tax planning and golden visas, were new to me.

Moreover, for every strict FIRE adherent I met, there was someone else in the movement who had bent or broken many of its rules to fit their own lifestyle goals. Many people don’t want to retire at all; they want to do meaningful work on their time and their terms.

Financial independence doesn’t have to mean not working. It’s simply about creating more streams of income in your life, which will give you more freedom and autonomy as a result.

FIRE is also in line with my personal finance editor ethos, which can be distilled down into eight words: Make more money, lower expenses, invest the difference. Follow those rules however you can, and your financial life will be on the right track.

Pro Tip:Personal finance, summarized in 8 words: “Make more money, lower expenses, invest the difference.”

Here’s an overview of the Financial Independence, Retire Early movement, where it came from, how it works, and ways to start implementing some or all its principles into your personal life.

Table of Contents

Summary of Financial Independence, Retire Early

- Calculate how much money you need in invested money to live off the annual interest gains alone.

- Determine how much you need to save and invest each month to reach this goal, based on how soon you want to stop working or producing income.

- Hit your monthly investing target by increasing your monthly income and/or decreasing your monthly expenses, then investing the excess.

- Adjust your goals as you go to ensure they inspire and challenge you, but don’t burn you out in the short term.

The Origins of the FIRE Movement

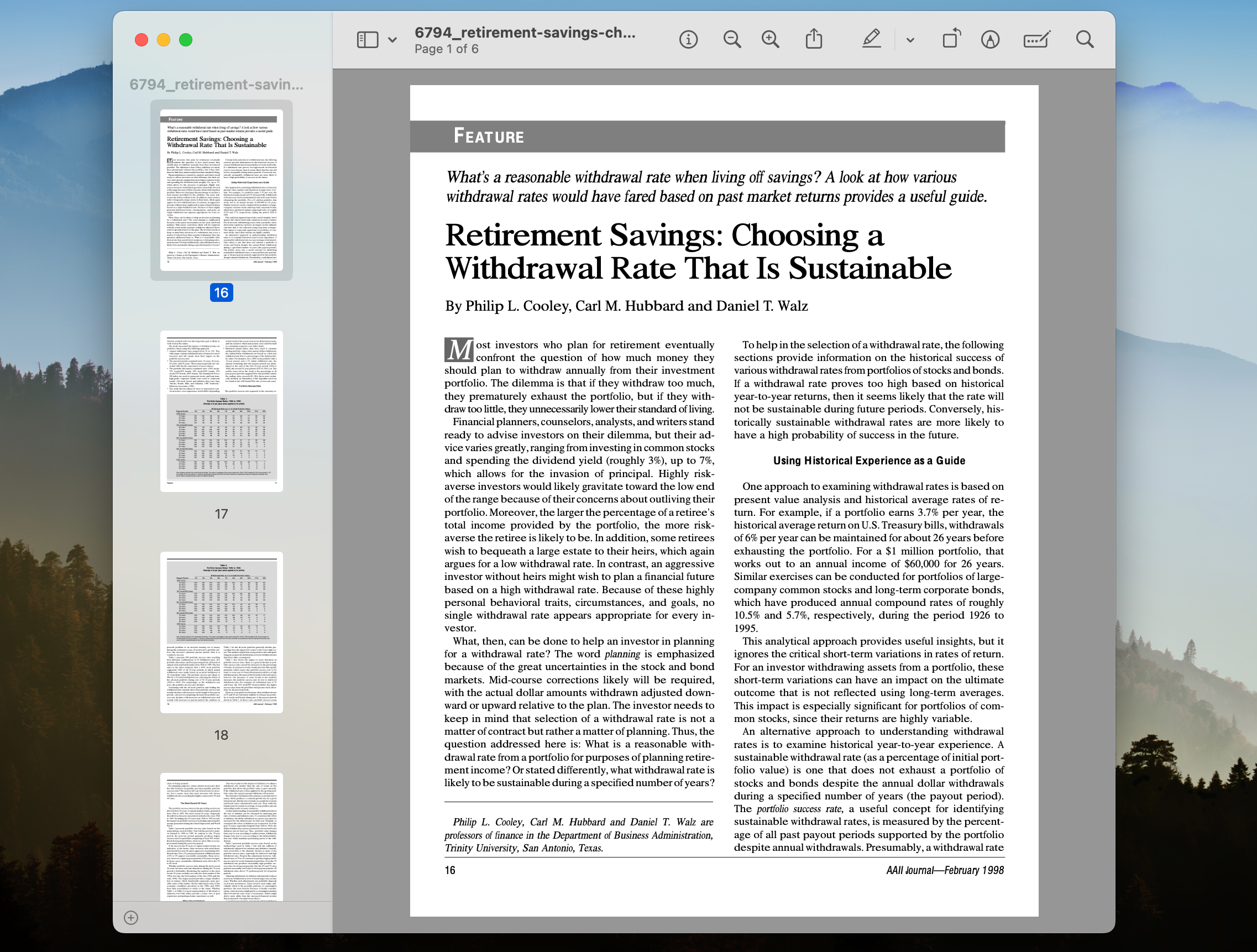

In 1998, three researchers at Trinity University published the results of a study on retirement savings.

Their projections found that, if an investor had a certain multiple of their income saved up and withdrew 4% or less of their nest egg each year, their chances of depleting their savings in a 30-year period were zero. Their research was based on rates of return since the invention of the 401(k) and other tax-advantaged retirement accounts, and later came to be known as the Trinity study.

The results of the Trinity study were first published in the American Association of Individual Investors Journal.

This research led to a reframe: If you could grow your nest egg large enough that the interest alone covered annual expenses and other medical expenses, most or even all of your principal would be protecting, preserving your wealth.

They Say Money Doesn’t Grow on Trees

But if your tree is a large-enough nest egg, well, it actually does. People began to realize that traditional retirement age wasn’t dictated by age, but whether you reach financial independence. Thus, the FIRE lifestyle was born.

FIRE stands for Financial Independence, Retire Early. Over the years, however, many FIRE followers began to break from core FIRE principles and define FIRE variations that better suit their lifestyle goals.

Key Takeaways

- Some FIRE devotees play for Fat FIRE, which requires a significant income on top of aggressive saving.

- Others prefer to pursue Lean FIRE, securing their financial future by lowering their expenses as much as possible in order to retire extremely early.

- Other offshoots don’t involve retiring at all; Coast FIRE focuses on hitting the number at which you know your nest egg will mature in time, and Barista FIRE is a milestone for those who want to keep working part-time or have residual side income.

Most FIRE enthusiasts aim to retire early, often in their 30s or 40s, by aggressively saving and investing as much money from their disposable income as they can. They max out contribution limits as part of their investing strategies, and may take on an additional part-time job or side hustle to reach their goals faster.

Key Idea:The pursuit of FIRE can instill good financial habits, even if you don’t actually want to retire early. As such, some FIRE participants cut the part about retiring early and just focus on financial security.

The Rules of Financial Independence, Retire Early

No. 1: Calculate Your Estimated FIRE Number

To reach financial security, you first have to figure out how much money you’ll need to consider yourself financially independent. One way to approximate this number is with the rule of 4, sometimes also known as the 4% rule.

This rule assumes that your investments will return 4% interest per year, which would be sufficient retirement income in FIRE. To calculate this, divide your anticipated annual expenses in retirement (or non-working lifestyle) by 0.04 (4%).

Another way to put this is to multiply anticipated annual expenses by 25.

Annual expenses x 25 = FIRE number (estimate)

It should be stated that this estimate is very rough and not entirely accurate.

- There will be inflation.

- If you’re in the US, there is Social Security.

- Some people will have pensions and royalties.

- Others will have unexpected medical debt or other financial setbacks.

- Did I mention inflation? Ah, I did. But here it is again for emphasis: Inflation.

In an October 1994 article for the Journal of Financial Planning, author Bill Bengen noted that inflation rates and withdrawals are never consistent, making this planning process more complex.

Remember that financial independence is a higher and more aggressive benchmark than plain-old retirement. You’re playing to reach a point of wealth at which dividends, investment withdrawals, and business owner draws can fully fund your lifestyle.

Lastly, it’s hard to predict where you’ll be in 20 or 30 or 40 years and how much your life will cost by then. But this number at least gets us started.

No. 2: Reverse-Engineer Your Savings Plan

Now we have to figure out how you’ll get to that number. You could just do some flat division, but remember that money you have saved in your bank account will grow and compound if you have it invested.

There are several free calculators online that will help you tinker with these concepts. Here is a simpler one from MoneyUnder30, and here is a more advanced one from WalletBurst.

No. 3: Close the Gap

To completely retire earlier than planned, you’ll almost certainly need to be saving thousands of dollars per month. You might already be doing this, but most people are not, and aren’t building enough wealth to ever reach their FIRE number.

The easiest way to close this gap is to go make more money. This could come in the form of online business efforts, side hustles, affiliate income, or many other streams. There is something for everyone.

You’ll also want to shore up your budgeting. Some Lean FIRE adherents will budget as tightly as possible to save money, but the tradeoffs might not be worth it for you. Nevertheless, it’s important to improve your financial education and spending habits so you don’t go off and blow all this extra money you’ve just worked so hard to make.

Lastly, know that most FIRE followers use investing in stocks, bonds, and index funds as their primary strategy to reach financial independence. If you take this strategy, put your money into tax-advantaged accounts or retirement accounts. Then make plans around how you will withdraw money later without accumulating penalties.

This blog is not investing advice; if you want to explore investing in more detail, start reading trusted publications online.

A screenshot of the vertical I oversaw as the financial independence editor for NextAdvisor, in partnership with TIME. Courtesy of Wayback Machine

Cultural Backlash to FIRE and Early Retirement

No. 1: Feasibility

While there are many FIRE followers, there are also many critics.

One of the main criticisms to FIRE is the high savings rate required to achieve financial independence. Saving 50% or more of one's income may be impossible for individuals and families, especially those with high living expenses or debt obligations. A six-figure salary for the household is often essential.

Additionally, critics argue that the FIRE movement often overlooks the possibility of unforeseen circumstances, such as medical emergencies or job loss, which can significantly impact a person's financial plans. By focusing solely on early retirement, individuals might neglect to build robust safety nets or prepare for unexpected events that could derail their long-term financial goals.

Many consumers struggle to pay taxes, grow an emergency fund, or get out from under high-interest debt, such as credit card debt. A Bankrate report found that 68% of Americans wouldn’t have enough savings to even last a month if they lost their source of income tomorrow.

Takeaway:Although financial freedom is a great motivator, the FIRE movement is sometimes panned as elitist and unrealistic.

No. 2: Is Doing Nothing Actually Fulfilling?

Another point of contention among skeptics is the concept of retiring early and completely leaving the workforce.

Critics argue that work holds value beyond just financial independence. It can provide a sense of purpose, social interaction, and continued feelings of contribution. They question whether a life without work, even if financially feasible, would truly lead to a happy and fulfilling retirement.

No. 3: Is the Short-Term Discomfort Worth It?

Moreover, skeptics argue that the aggressive savings and investment strategies required to achieve FIRE can diminish your present-day quality of life.

Extreme budgeting can strain relationships and create tunnel vision regarding life goals. Critics suggest that finding a balance between enjoying the present moment while still working towards long-term goals might provide a more sustainable approach to personal finance.

Frequently Asked Questions

What Does FIRE Stand For in Personal Finance?

FIRE stands for Financial Independence, Retire Early, and refers to a wealth benchmark at which you can become work-optional.

How Much Do You Need to Retire FIRE?

A first benchmark for Americans is 25x your annual expenses. Based on Census data, this means having between $1 million and $2.5 million in invested assets for most people.

What Is the 4 Rule for Retirement?

The 4 rule, also called the rule of 4 or the 4% rule, asserts that an annual withdrawal of 4%, adjusted for inflation, is a safe withdrawal rate for 30 years of retirement.

What Is the 25x Rule?

The 25x rule says that multiplying your annual expenses by 25 gives you a minimum benchmark at which you would be able to live mostly or fully off of yearly investment gains alone.

How Do You Calculate FIRE?

To calculate a rough FIRE number, multiply your annual expenses by 25. For a more conservative number, multiply by 33.

How Much Do You Need for Financial Independence, Retire Early?

The amount varies widely, and is based on your cost of living. Most FIRE devotees will need to save at least $1 million-$2.5 million.

How Does the FIRE Movement Work?

Make more money through multiple streams of income, reduce your living expenses, and save and invest your money to increase wealth over time.

Is the FIRE Movement Realistic?

For many, FIRE is too aggressive. It often requires saving over 50% of your income. Viable solutions are to increase income, lower expenses, or redefine lifestyle goals.

Are There Specific FIRE-Friendly Investments?

Popular investment options include low-cost index funds and rental properties. A business can also be a FIRE-friendly investment.

Where Should I Invest for FIRE?

Prioritize tax-advantaged accounts first. These accounts will provide tax breaks on your gains that don’t apply in a regular investment brokerage.

Final Takeaway

If you’re trying to make money online, increase your income, or design a certain lifestyle, you’re already a part of the FI movement.

Decide how you want to live in the future, then start taking action today to bring those plans to fruition, one dollar at a time. ◆

Thanks For Reading 🙏🏼

Keep up the momentum with one or more of these next steps:

📣 Share this post with your network or a friend. Sharing helps spread the word, and posts are formatted to be both easy to read and easy to curate – you'll look savvy and informed.

📲 Hang out with me on another platform. I'm active on Medium,Instagram, and LinkedIn – if you're on any of those, say hello.

📬 Sign up for my free email list. This is where my best, most exclusive and most valuable content gets published. Use any of the signup boxes on the site.

🏕 Up your writing game. Camp Wordsmith® is a content marketing strategy program for small business owners, service providers, and online professionals. Learn more here.

📊 Hire me for consulting. I provide 1-on-1 consultations through my company, Hefty Media Group. We're a certified diversity supplier with the National Gay & Lesbian Chamber of Commerce. Learn more here.